Practical Ideas On How To Fight The Twin Evils Of: Junk Mail and Credit Card Offers

I don't particularly mind receiving mail and catalogs from companies I've chosen to do business with in the past. It disturbs me when a company I've done business with decides they haven't made enough off of me already and so, in order to maxamize their profits, they feel the need to sell my name to the whole rest of the world. I really do not care for unsolicited "junk mail," especially offers to sell myself into financial slavery and bondage.

The number of

unsolicited credit card solicitations that the average American receives is

disgusting. I suppose I really ought to start counting how many I receive,

but I'd hazard a guess that I (and those in my immediate household) receive

a dozen or so per month--possibly more.

The number of

unsolicited credit card solicitations that the average American receives is

disgusting. I suppose I really ought to start counting how many I receive,

but I'd hazard a guess that I (and those in my immediate household) receive

a dozen or so per month--possibly more.

In either January or February of 1998 the Wall Street Journal had a small feature article about a woman who had kept track of the total dollar value of all credit card offers her family had received during 1997. As I recall it was something along the lines of $3,500,000. . . . That is a lot of money! (To make use of that amount of credit, you'd have to charge almost $10,000 per day, each & every day of the year. . .)

The credit card offers always like to tell you about what a responsible person you are, and how, since you have such good credit, they'd be oh-so willing to lend you $5,000 or $10,000 at a "low" rate of 14% to 23%. Translated: Our computerized search of the records of the nation's largest credit buereaus has identified (from the information in your "private" files), the fact that you've been a fool enough to pay hundreds of dollars in interest to other credit card companies (instead of just deferring your purchases long enough to save up a bit of money)--and so you're just the kind of idiot our statistical models tell us we'd like to have as a customer.

Although I don't often receive them, offers for "secured credit cards" really make me sick. They want you to send in $500 to $1,000 as a "security deposit," and they'll then issue you a credit card with a $500 to $1,000 limit. They'll pay you 2.1% on your "deposit" and then charge you 21% on any balance you carry on your credit card. For the "risk" they incur lending you your own money, they earn a 19% spread. A real scam in my opinion.

I've read

that a 2% response rate for a direct mail campaign is considered very

succesful. That means that only one person actually responds for every

49 of us that end up throwing the junk mail in the trash. Although I'm

not a tree-hugger by any stretch of the imagination, that does seem

like an awful lot of wasted resources, even if you were only to consider the

time of the recipient, let alone the paper, ink, & postage expended by

the sender.

I've read

that a 2% response rate for a direct mail campaign is considered very

succesful. That means that only one person actually responds for every

49 of us that end up throwing the junk mail in the trash. Although I'm

not a tree-hugger by any stretch of the imagination, that does seem

like an awful lot of wasted resources, even if you were only to consider the

time of the recipient, let alone the paper, ink, & postage expended by

the sender.

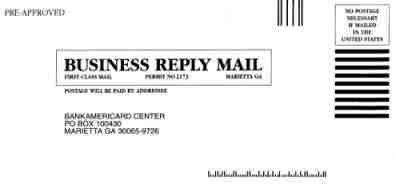

My solution to the problem of junk mail:

Send it right back! Direct mail solicitors waste my time; when they are so generous to pick up the return postage, why not waste a bit of theirs?

If they can send me junk, I'll send them junk back. (Maybe the junk mailers will feel all warm & fuzzy when their response rate goes up from 2% to 3% . . .)

Maybe the kind people at

Bank of America who sent

me a really nice letter informing me that they were willing to let

me transfer up to $7,000 from my other credit cards (at a "low" teaser

rate of 9.9%, which would jump to the prime rate + 8.99% in a few months)

would appreciate saving a few bucks on pizza. Now I'm not real sure

that this coupon would do them much good in either California (the return

address on their letter), or in Georgia (the destination address on their

business reply mail envelope)--since this coupon is for

a local pizza

place here in Utah (and, actually, only at their locations in Bountiful

& Layton to boot) . . . but you never know. I suppose it

is the thought that really counts.

Maybe the kind people at

Bank of America who sent

me a really nice letter informing me that they were willing to let

me transfer up to $7,000 from my other credit cards (at a "low" teaser

rate of 9.9%, which would jump to the prime rate + 8.99% in a few months)

would appreciate saving a few bucks on pizza. Now I'm not real sure

that this coupon would do them much good in either California (the return

address on their letter), or in Georgia (the destination address on their

business reply mail envelope)--since this coupon is for

a local pizza

place here in Utah (and, actually, only at their locations in Bountiful

& Layton to boot) . . . but you never know. I suppose it

is the thought that really counts.

By my calculations, it will cost Bank of America at least 42¢ to receive my junk response. The United States Postal Service charges 32¢ for first class postage, plus a 10¢ handling fee for business reply mail. (The USPS posts their rate information online.) If I were to send them a lot of coupons, it could cost them even more: 23¢ for each additional ounce. But at least they'll save $4.00 on their pizza . . .

The following is true of both credit card

solicitations, and all other forms on obnoxious, unsolicited, unwanted

junk-mail: If the 98 out of 100 people who end up tossing junk mail were to

respond in such a thoughtful manner as I always try to do, it would

cost the junk mailers an additional $21.00 (plus whatever it costs them

to process replies) to dig through the "junk" and find the one really

interested respondent. (I don't think this even begins to compensate for

the value of my time that they waste. If they are going to make the

signal to noise ratio higher for our mailboxes, let's do the same

for theirs.) If everyone did sent a junk reply to every piece of

unsolicited junk mail they received, I imagine our land fills would last

a lot longer . . .

The following is true of both credit card

solicitations, and all other forms on obnoxious, unsolicited, unwanted

junk-mail: If the 98 out of 100 people who end up tossing junk mail were to

respond in such a thoughtful manner as I always try to do, it would

cost the junk mailers an additional $21.00 (plus whatever it costs them

to process replies) to dig through the "junk" and find the one really

interested respondent. (I don't think this even begins to compensate for

the value of my time that they waste. If they are going to make the

signal to noise ratio higher for our mailboxes, let's do the same

for theirs.) If everyone did sent a junk reply to every piece of

unsolicited junk mail they received, I imagine our land fills would last

a lot longer . . .

All of this is just food for thought. Pizza anyone?

— Michael A. Cleverly

Saturday, August 15,

1998

43 comments

| Printer friendly version